by Russell Noga | Updated November 22nd, 2023

What Are the Disadvantages of a Medicare Supplement Plan?

Navigating the world of Medicare coverage can be daunting, especially when it comes to understanding the various supplemental insurance options available.

While Medicare Supplement Plans, also known as Medigap plans, offer valuable coverage to fill in the gaps of Original Medicare, they come with their own set of disadvantages.

What are the disadvantages of a Medicare Supplement Plan? Are these drawbacks significant enough to deter you from choosing a Medigap plan? Let’s delve into the details and find out.

Short Summary

- Medigap plans are supplemental insurance policies that cover gaps in Original Medicare but can be expensive and lack additional benefits.

- When selecting a Medigap plan, consider healthcare needs, financial situation, provider preferences and compare coverage options.

- Rates for Medigap plans may increase due to various factors. Proactively comparing rates and exploring alternative coverage options is recommended to manage rate increases.

Understanding Medicare Supplement Plans

Medicare Supplement Plans, also known as Medigap plans, are supplemental insurance policies issued by private insurance companies.

These plans help fill gaps in coverage that Original Medicare doesn’t cover. A Medicare supplement insurance plan is designed to assist in covering additional medical costs that Original Medicare does not cover, such as copayments, coinsurance, and deductibles. One option to consider is a Medicare supplement plan, which can provide tailored coverage to suit your needs.

While Medigap plans can provide valuable coverage and peace of mind, they also come with certain drawbacks, which we will explore further in this article.

What is a Medigap Plan?

A Medigap plan is a supplemental insurance policy specifically designed to supplement Original Medicare coverage. Eligibility to acquire Medigap policies for individuals below 65 varies by state, and the six-month open enrollment period for these policies commences during the initial six months following enrollment in Medicare Part B at age 65 or older.

Factors such as age, postal code, and plan selection influence the cost of Medigap plans.

Compare Rates Now

Enter Zip Code

Types of Medigap Plans

There are 10 standardized Medigap plans, each offering different levels of coverage and benefits.

These lettered plans (A, B, C, D, F, G, K, L, M, and N) provide coverage for the gaps in Original Medicare, making it easier for seniors to manage their healthcare expenses with reduced out-of-pocket costs.

However, it is important to note that prescription drug coverage is not covered by Medigap plans. Instead, seniors can acquire a separate Medicare Part D plan to supplement prescription coverage if needed.

Disadvantages of Medicare Supplement Plans

Understanding the potential drawbacks of Medigap plans is essential to make an informed decision regarding your healthcare coverage.

Some of the most notable disadvantages include high monthly premiums, limited guaranteed enrollment periods, and a lack of additional benefits like vision, dental, or prescription drug coverage.

Let’s explore these disadvantages in more detail.

High Monthly Premiums

Medigap plans can be expensive, with monthly premiums varying based on factors such as:

- age,

- location,

- and plan type.

While these plans can help reduce out-of-pocket expenses for seniors, the high monthly premiums can be a financial burden.

For example, the estimated cost of a Medigap Plan G policy for a 65-year-old woman residing in Tampa, Florida in 2023 is approximately $180 per month. Therefore, it is crucial to weigh the cost of Medigap plans against the potential savings in out-of-pocket expenses.

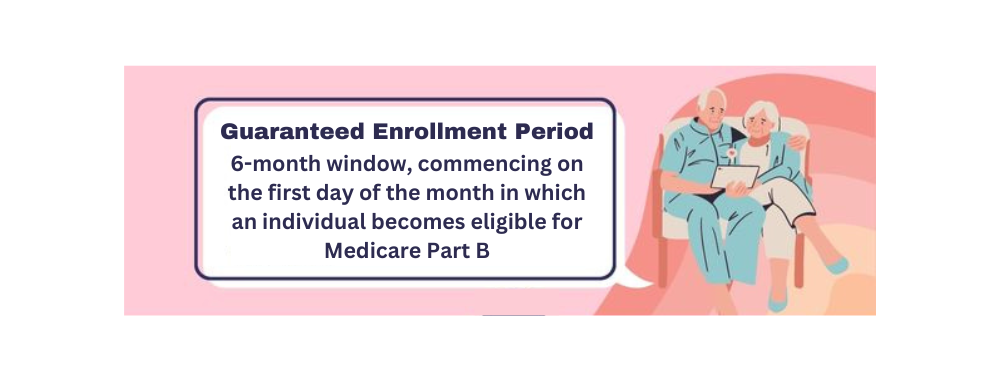

Limited Guaranteed Enrollment Period

The guaranteed enrollment period for Medigap plans is limited to a six-month window, commencing on the first day of the month in which an individual becomes eligible for Medicare Part B.

During this period, individuals are entitled to purchase any Medigap policy available in their state, regardless of their health condition.

However, after this six-month window, insurers may refuse coverage based on medical underwriting, which evaluates an individual’s medical history to determine their eligibility for a Medigap plan.

This can result in individuals with pre-existing conditions being denied coverage or charged higher premiums.

Lack of Additional Benefits

One notable drawback of Medigap plans is the lack of additional benefits that many Medicare Advantage plans offer.

Medigap plans do not typically include vision, dental, and hearing services as additional benefits. This means that seniors who require these services may need to seek separate coverage or pay for these expenses out-of-pocket.

In the debate of Medicare Advantage vs traditional Medicare, Medicare Advantage plans often provide a more comprehensive package of benefits, including prescription drug coverage and additional services like vision, dental, and hearing.

Comparing Medigap and Medicare Advantage

When deciding between Medigap and Medicare Advantage, it is essential to compare:

- the coverage,

- provider networks,

- and costs associated with each option.

While Medigap plans can minimize out-of-pocket expenses, they may not provide the comprehensive coverage and additional benefits that many Medicare Advantage plans offer.

In this section, we will explore the differences between Medigap and Medicare Advantage plans in more detail.

Coverage Differences

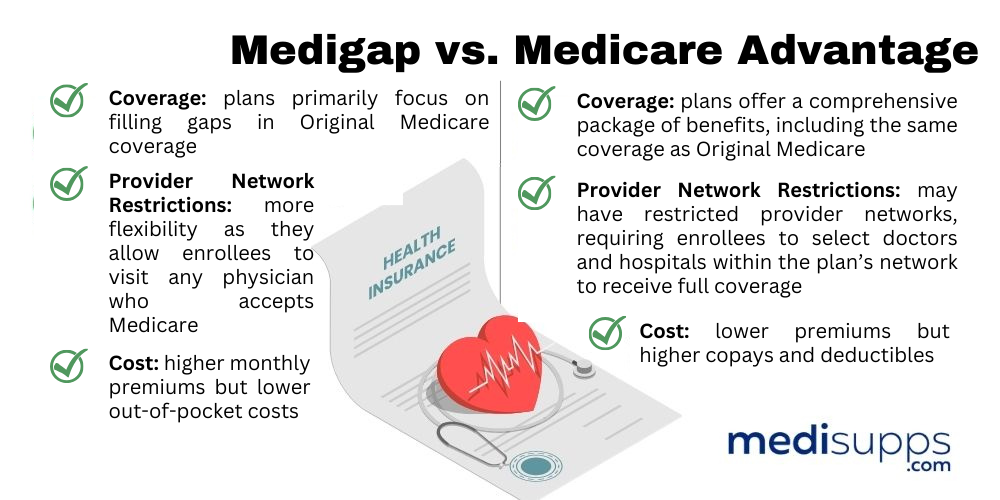

Medigap plans primarily focus on filling gaps in Original Medicare coverage, such as copayments, coinsurance, and deductibles. These plans do not provide coverage for additional services like prescription drugs, vision, dental, hearing, and other wellness services.

On the other hand, Medicare Advantage plans offer a comprehensive package of benefits, including the same coverage as Original Medicare, as well as extra benefits like prescription drug coverage and additional services like vision, dental, and hearing.

One option to consider is a Medicare Advantage Plan, which provides these added benefits within a single plan.

Provider Network Restrictions

When it comes to provider networks, Medigap plans offer more flexibility as they allow enrollees to visit any physician who accepts Medicare.

In contrast, Medicare Advantage plans may have restricted provider networks, requiring enrollees to select doctors and hospitals within the plan’s network to receive full coverage. Out-of-network coverage may be available in some plans but at a higher cost.

It is crucial to evaluate the plan’s network and coverage options before enrolling.

Cost Considerations

When comparing costs, Medigap plans generally have higher monthly premiums but lower out-of-pocket costs.

In contrast, Medicare Advantage plans typically have lower premiums but higher copays and deductibles. The average monthly premium for Medigap plans in 2022 was reported to be $128 per month, while the cost of Medicare Advantage plans can range from $0 to over $300 per month, depending on the coverage and benefits provided.

It is essential to weigh the costs against the benefits and coverage offered by each plan to determine the best option for your unique needs.

Navigating Medigap Plan Options

Choosing the right Medigap plan can be a daunting task, as there are 10 standardized plans available, each with varying levels of coverage and benefits. To make the best decision, it is crucial to consider factors such as coverage needs, budget, and provider preferences.

In this section, we will offer guidance on navigating Medigap plan options and selecting the best plan for your needs.

Factors to Consider

When selecting a Medigap plan, it is important to consider your individual healthcare needs, financial situation, and provider preferences. For example, if you have a chronic condition that requires frequent medical care, you may want to prioritize coverage for copayments, coinsurance, and deductibles.

On the other hand, if you are relatively healthy and do not anticipate significant medical expenses, a plan with lower premiums and fewer benefits may be more suitable. It is also essential to consider the providers in the plan’s network, as some plans may impose limitations on the services they render or the types of plans they accept.

Shopping for Medigap Plans

When shopping for a Medigap plan, it is crucial to compare different plans to ensure that you are getting the most suitable coverage for your needs. Some tips for comparing and selecting Medigap plans include:

- shopping around,

- contacting insurance companies licensed in your state,

- and enlisting the aid of an insurance agent to help you compare plans.

Additionally, it is important to understand the differences between Medigap plans, including the coverage they offer, any restrictions or limitations that may apply, and the cost of the plan.

By thoroughly researching and comparing plans, you can make an informed decision and select the best Medigap plan for your unique needs.

Medigap Coverage for Pre-Existing Conditions

Understanding how Medigap plans handle pre-existing conditions is essential, as it can impact your coverage and premium rates. Medigap plans do not offer coverage for pre-existing conditions, but they do provide coverage for any medical conditions that may manifest after the policy has taken effect.

In this section, we will discuss the importance of guaranteed-issue rights and how they protect individuals with pre-existing conditions from being denied Medigap coverage.

Guaranteed-Issue Rights

Guaranteed-issue rights are a set of protections that prevent insurance companies from denying coverage to individuals with pre-existing conditions during the open enrollment period.

Guaranteed-issue rights are a set of protections that prevent insurance companies from denying coverage to individuals with pre-existing conditions during the open enrollment period.

These rights ensure that individuals can purchase any Medigap policy available in their state, regardless of their health status, and cannot be charged higher premiums based on their medical history.

Understanding and taking advantage of guaranteed-issue rights can help individuals with pre-existing conditions secure the coverage they need without facing discrimination or higher premiums.

Medical Underwriting

After the open enrollment period, an insurance company can use medical underwriting to determine eligibility and premium rates for Medigap plans. This process involves reviewing an individual’s medical history and health status to assess the risk of insuring them and guarantee the financial stability of the plan.

As a result, individuals with pre-existing conditions may be denied coverage or charged higher premiums after the open enrollment period. It is essential to be aware of your guaranteed-issue rights and explore options for coverage if you have a pre-existing condition and are considering a Medigap plan.

Medigap Plan Costs and Rate Increases

Understanding the factors that influence Medigap plan rate increases is crucial, as it can help you better manage your healthcare expenses. In this section, we will explore the factors that can lead to rate increases, such as age, location, and the overall health of plan enrollees.

Understanding the factors that influence Medigap plan rate increases is crucial, as it can help you better manage your healthcare expenses. In this section, we will explore the factors that can lead to rate increases, such as age, location, and the overall health of plan enrollees.

We will also offer tips for managing these increases.

Factors Influencing Rate Increases

Several factors can impact rate increases for Medigap plans, including:

- Location

- Age

- Tobacco use

- Payment method

- Inflation

- General rise in healthcare costs

For example, older individuals are more likely to require medical care, leading to higher premiums.

Additionally, certain areas may have higher healthcare costs, resulting in increased rates for Medigap plans. Understanding the factors that can lead to rate increases can help you better anticipate and manage your healthcare expenses.

Tips for Managing Rate Increases

To manage Medigap plan rate increases, consider shopping around and comparing rates from different insurance companies to find the best deal. Additionally, take advantage of any available discounts, such as those for individuals aged 65 and above or those with specific medical conditions.

If you find that Medigap plan rates are too high, consider exploring alternative coverage options, such as Medicare Advantage plans or employer-sponsored plans.

If you find that Medigap plan rates are too high, consider exploring alternative coverage options, such as Medicare Advantage plans or employer-sponsored plans.

By being proactive in managing rate increases, you can ensure that you have the coverage you need at a price you can afford.

Summary

In conclusion, while Medigap plans can provide valuable supplementary coverage to fill gaps in Original Medicare, they also come with several disadvantages, including high monthly premiums, limited enrollment periods, and a lack of additional benefits.

By understanding the differences between Medigap and Medicare Advantage plans, considering factors such as:

- coverage needs,

- budget,

- and provider preferences,

- and exploring alternative coverage options, you can make an informed decision and choose the best healthcare plan for your unique needs.

Remember, the key to finding the right plan lies in diligent research, comparison, and understanding your personal healthcare requirements.

Get Quotes in 2 Easy Steps!

Enter Zip Code

Frequently Asked Questions

Is Medicare with a supplement more expensive than a Medicare Advantage?

Generally, Medicare Advantage plans are more cost-effective than Original Medicare plus a supplement, as monthly premiums may range from $0 to $100, while Supplement coverage may go from $50 to $1,000 per month.

Additionally, out-of-pocket costs tend to be lower in a Medicare Advantage plan.

Can Medicare Supplement plans turn you down?

No, Medicare Supplement plans cannot turn you down during the Open Enrollment period, regardless of pre-existing medical conditions.

Why would someone choose a Medicare Supplement Plan A?

Medigap Plan. A is a great option for those seeking to reduce out-of-pocket costs associated with Original Medicare as it helps cover expenses like copayments, coinsurance and deductibles.

Additionally, it can also provide coverage for home healthcare, durable medical equipment, hospital costs and lab costs.

What is the main difference between Medigap and Medicare Advantage plans?

Medigap plans are designed to supplement Original Medicare coverage, while Medicare Advantage plans provide additional benefits and services beyond Original Medicare.

How can I manage Medigap plan rate increases?

To manage Medigap rate increases, shop around and compare rates, take advantage of discounts, and explore alternative coverage options.

Look for insurers that offer discounts for couples, those who pay their premiums in full, and those who are members of certain organizations. Consider alternative coverage options such as Medicare Advantage plans, which may offer lower premiums.

Find the Right Medicare Plan for You

Finding the right Medicare Plan 2024 doesn’t have to be confusing. Whether it’s a Medigap plan, or you want to know more about Medicare Supplement Plans, we can help.

Call us today at 1-888-891-0229 and one of our knowledgeable, licensed insurance agents will be happy to assist you!

Russell Noga is the CEO and Medicare editor of Medisupps.com. His 15 years of experience in the Medicare insurance market includes being a licensed Medicare insurance broker in all 50 states. He is frequently featured as a featured as a keynote Medicare event speaker, has authored hundreds of Medicare content pages, and hosts the very popular Medisupps.com Medicare Youtube channel. His expertise includes Medicare, Medigap insurance, Medicare Advantage plans, and Medicare Part D.